I am excited to kick off a new blog series of mine. The topic? You have guessed correctly: Embedded Finance (EF). Every week I will post about a particular EF topic. It's what I refer to as The Embedded Finance Guide. But why am I doing this?

As some of you may recall, I joined Weavr in the fall of 2020 (blog post) after about one and a half years of working as a freelance Fintech consultant. I enjoyed the versatility of being a freelancer, but my expectations for EF were massive (and still are). That’s why it was an easy decision to join Weavr when I understood how the team was planning to address the needs of the upcoming solutions.

I've talked to dozens of tech companies since joining Weavr that were considering to expand their current offering to include financial products. I have a similar target group in mind for my blog post series. As a result, the posts will be directed at those who are developing EF products at their organizations rather than Fintech nerds. I will concentrate on issues that are relevant to the European market, however, I may sporadically utilize examples from other areas.

Please ping me if you have any specific queries or subjects you'd like me to address. Based on conversations I've had in recent months, my current list of themes is as follows:

- EF vs Open Banking

- EF vs Vertical Banking

- Why is EF happening now?

- Why should you do EF?

- How to make money with EF?

- What paths can you go to build EF?

- In which area will EF have the biggest impact?

When is it EF and when not?

EF is currently one of the most used buzzwords in Fintech. The term is used by numerous businesses, organizations, or "influencers," and these parties frequently misuse it. However, it is hard to blame them as the space is complex, evolving quickly and driven by various stakeholders with different intentions or approaches.

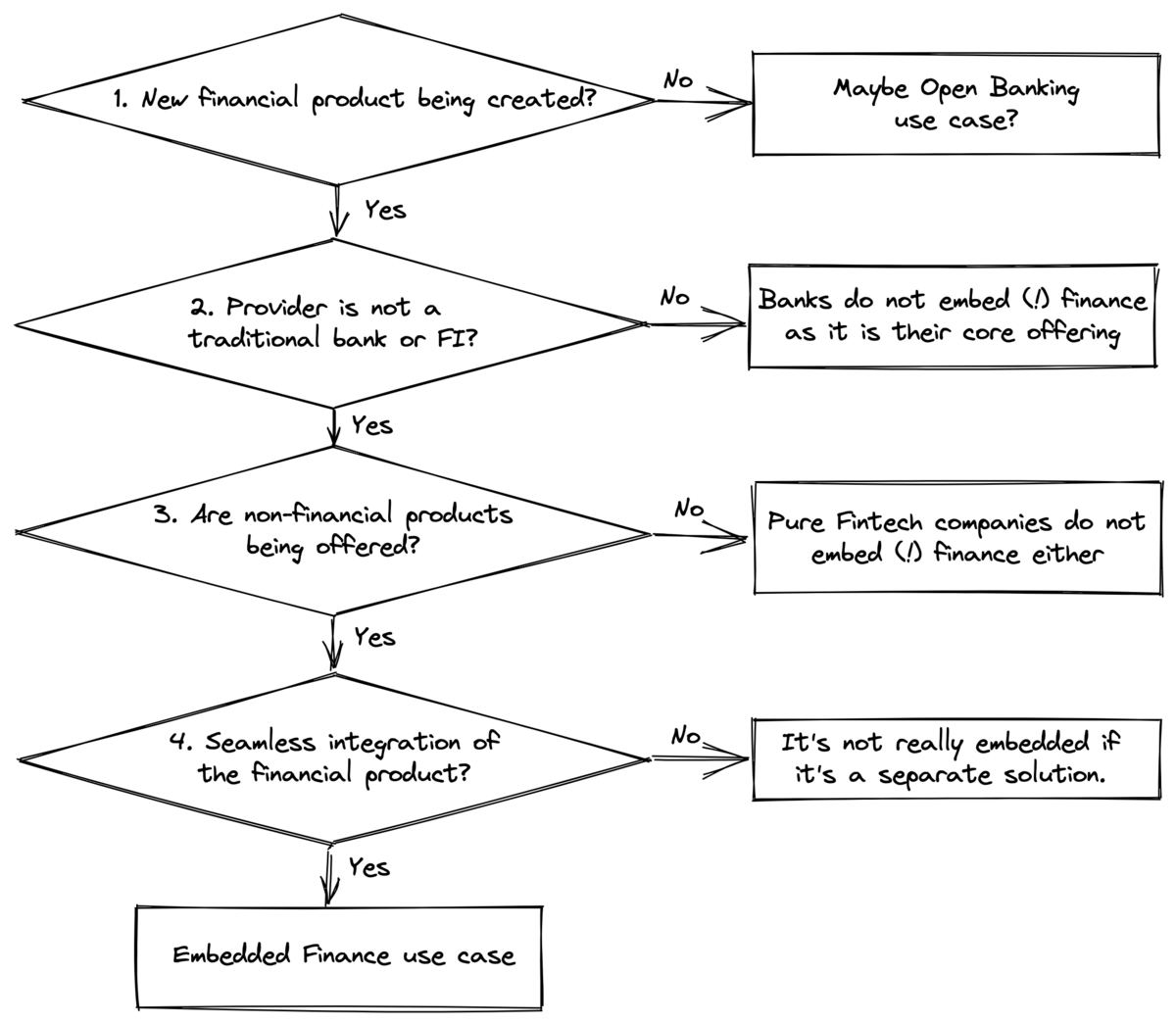

Also not every financial services needs to be consumed in an EF way - at least today. ;) When I examine a new offering and consider whether it falls under the EF category, I typically ask myself the following questions:

- Is a new financial product (such as a bank account, credit card, or loan) being created?

- Is the business delivering this financial product not a traditional bank or financial institution?

- Does the business offer non-financial products as well?

- Is the financial product offering integrated seamlessly into the customer journey?

The flow in my head looks more or like this:

Personally, I would classify a product only as an EF solution if the answers to all of these questions are answered with “yes”. However, it can be a bit tricky and there may be different interpretations - especially for the very last question. Let me describe you what I mean: There are examples of non-banks (Question 2) creating new financial products (Question 1) while also offering other non-financial products (Question 3) but without a seamless integration of the financial product (Question 4). For example, there are different companies in Germany (including Amazon) that are offering a Credit Card via a partnerbank. However, the user cannot manage or access card details inside the normal Amazon website but has to use a separate portal provided by the partnerbank. While these business reap some of the benefits of an EM solution, it is not a full-fledged EF solution. In such a solution, the user still has to navigate different tools which could be compared with using a non-financial solution in combination with a traditional banking solution.

That being said, I agree that there is a fine line when a non-bank introduces a financial product through a separate app or website for agility reasons. It might be the right approach for some businesses to start with a separate financial app or website and iterate fast without any limitation from the core business. Nevertheless, there should be the goal that the financial product will later be incorporated into the primary service (obviously something which cannot be judged from the outside). So while the above questions and graphic might help with the EF classification, a subjective close look may always be required.

What are great examples of EF solutions?

I have been asked often what my favorite examples of EF are, and while there are many good ones, I often use the following three to highlight different angles of EF:

- Lyft is providing a debit card solution to their drivers which enables the driver to get paid instantly after every ride. Uber had a similar offering at one point. While the banking solution of Shopify is slightly different, it follows the same characterics.

- 1Password is offering a virtual card solution (via Privacy) that enables users to create a new card for every subscription they are signing up for (US only).

- Grover launched its debit card solution in Germany which is the core pillar of its loyalty program that aims to increase tech/gadget subscriptions per customer.

I hope you enjoyed reading this light and very first post of my EF blog post series. Please share any feedback you might have (negative feedback highly appreciated!). Feel free to use the new subscribe feature I added to my blog, so you can make sure not to miss the next post of Embedded Finance Guide. See you next week!