Hi from Berlin,

Welcome to a fully packed newsletter. Before we dive into the stories, there are three things from my side:

Embedded Finance Report: APIdeck published an extensive report, which I contributed to. It examines how different industries adopt embedded finance, includes our survey results, and features hundreds of relevant providers across the main categories. Read it here

Virtual Event: Virtual Events are back, this time with a proper conversation about embedded lending. I am sitting down with Temi Ofong (HSBC) and Nicolas Kipp (Credibur) on a 60-minute video call. We will go deep on whether embedded lending actually moves GMV, why growth so often plateaus after launch, and what it takes to hit the volumes people keep predicting. Spots are limited. Register here

Fintech Drinks and Stories @ Berlin: We are hosting our casual evening with our friends from Airwallex, Debtist, and House of Finance & Tech on Thursday (June 11th). If you are in Berlin, join us for drinks, food, and good conversations. Register here

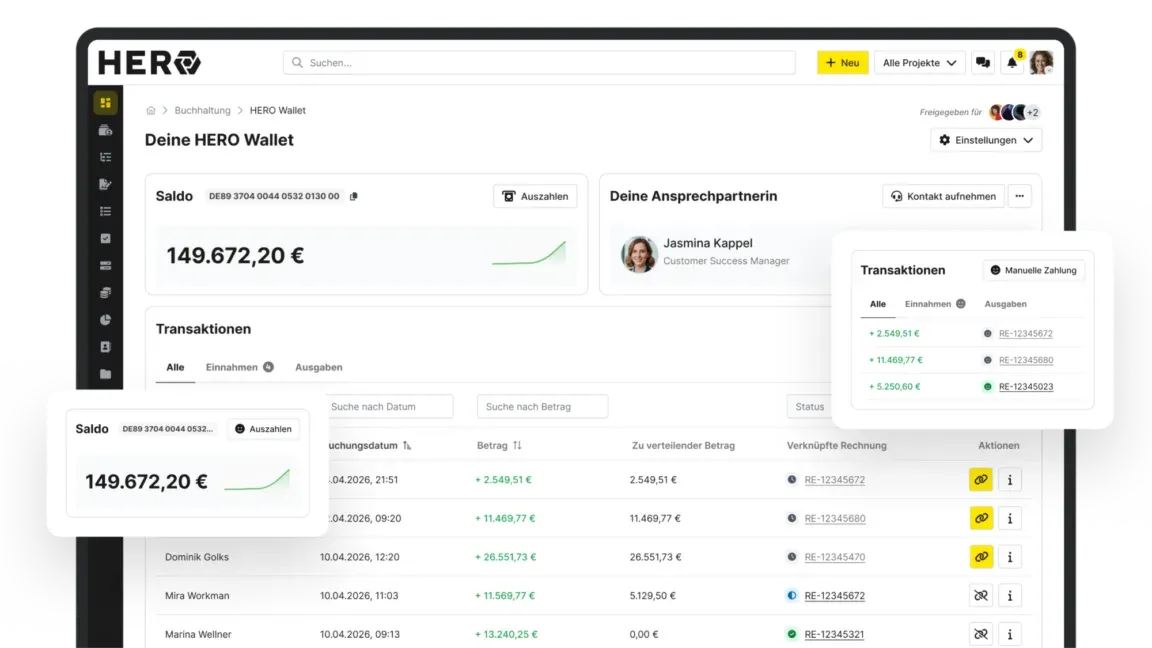

HERO Software launches HERO Wallet with Swan for German craftsmen

HERO Software has launched HERO Wallet, an embedded payments and reconciliation product for craft businesses in Germany. HERO is a vertical SaaS for the craftsmen sector, founded in 2020 in Hannover, with around 40,000 users across plumbing, sanitary, electrical, roofing, and other trades. The company operates across Germany, Austria, and Switzerland, and the typical customer is a small to mid-sized craft business with two to fifty employees. With HERO Wallet, each customer of a craft business gets their own virtual IBAN(s). Incoming SEPA payments are automatically reconciled against the right invoice, open items are kept current, and the integrated dunning workflow takes over if a payment is late. The whole thing lives inside the HERO software, where the craft business already quotes, manages jobs, and invoices. Deposits are held with Swan, a French licensed e-money institution.

HERO is not the first company in this space. In Germany, the closest comparable is ToolTime, which did something structurally similar in the German craft market when it launched ToolTime Pay with Adyen in 2024. The international role model is ServiceTitan in the United States, the dominant vertical SaaS for home services trades, which has been layering financial services onto its core workflow product for years through ServiceTitan Payments and ServiceTitan Financing. The German craft market receives less international attention because its customer base is small, German, and offline, but it is one of Europe's larger underserved verticals, with around 570,000 craft businesses in Germany alone. HERO already covers a meaningful share of that market with 40,000 users and is now adding the financial layer on top.

Read the full story on Embedded Finance Review

ryd launches fleet payments with Mastercard, expanding from consumer to B2B

ryd, the Munich-based mobility payments company, has launched ryd fleet in collaboration with Mastercard, expanding from its consumer base into the European B2B fleet market. ryd was founded in Munich in 2014 and operates Europe's largest cross-brand mobile payment network at fuel pumps, with more than one million consumer users across Germany, Austria, Switzerland, Benelux, Denmark, Portugal, and Spain. The platform is natively integrated into Audi, BMW, Mercedes-Benz, and Skoda infotainment systems, and strategic investors include BP, Mercedes-Benz, AXA, and Mastercard. With ryd fleet, drivers pay for fuel, EV charging, car washes, and other vehicle expenses through the ryd app or directly through their vehicle's infotainment system, using a tokenised virtual Mastercard. Acceptance follows Mastercard's commercial card network across Europe, which is significantly broader than the closed-loop networks traditional fleet cards rely on. Fleet managers get a portal with near real-time transaction data and spend controls by category, driver, or vehicle.

ryd is not a non-financial brand that added a payment product, since payments have been ryd's core product since 2014. Nevertheless, solutions like ryd in the mobility and fuel payments space have traces of Embedded Finance. And the more interesting question is how a consumer payments business graduates into B2B. The consumer app proved the in-car payment behaviour. The OEM integrations gave ryd distribution into millions of vehicles, and the existing service station relationships gave ryd acceptance density. Now ryd is applying all three to fleet, which is a market segment with very different economics: B2B customers buy in volume, sign multi-year contracts, and value data and controls as much as acceptance.

Read the full story on Embedded Finance Review

Why German banks lose €1 billion a year to the last mile

Germany sent €22.3 billion in remittances in 2024, making it the fourth-largest sending country in the world behind the US, Saudi Arabia, and Switzerland. Almost none of that volume runs through the banks that German senders hold their primary accounts with. A new Thunes report puts the annual gross revenue captured by non-bank money transfer operators at roughly €1 billion, and frames the gap as an infrastructure problem rather than a demand problem. A typical sender opens their German banking app to send €200 to family in Kenya or the Philippines, but sending directly to an M-Pesa or GCash wallet is not an option. So the sender leaves the app, opens Wise or Remitly, and funds the transfer from the same German account they just closed. From that point on, the bank is just the funding source. Everything that makes the transaction valuable, the FX margin, the fees, the data, and the recurring customer relationship, sits with the Money Transfer Operator (MTO).

The structural reason banks struggle to compete is that the market's receiving end has shifted. Account ownership in developing economies rose from 54% in 2011 to 71% in 2021, but most of that growth came through mobile wallets rather than bank accounts. bKash in Bangladesh, M-Pesa in Kenya, and GCash in the Philippines now function as the primary financial account for hundreds of millions of people. A German bank's correspondent rails are built for IBAN-to-IBAN transfers, not for wallet payouts. The technical challenge has a name: account-to-wallet, or A2W. It sits next to the more familiar account-to-account (A2A) model that underpins SEPA and most domestic European payments. A2W means a payment originates from a bank account in one country and lands directly in a mobile wallet in another, without the sender or recipient needing to touch an MTO in the middle.

Read the full story on Embedded Finance Review

In other Embedded Finance news

- Wallester has received FCA authorisation as an Electronic Money Institution in the UK: The Tallinn-headquartered card-issuing and embedded finance platform now operates a regulated UK entity led by CEO Julian Brand. The UK operation focuses on Wallester Business (corporate expense management) and Wallester White-Label (card issuing and embedded finance for regulated partners and corporate brands). (FF News)

- Equals Money and Railsr complete merger and rebrand as Equals: The combined business is now positioned as a global money movement and embedded payments platform, processing £58 billion in transaction volume in 2025/26. The rebrand consolidates two of the UK's better-known embedded payments names into one platform offering accounts, cards, FX, and embedded payment infrastructure for business clients. (FX News Group)

- IKEA Italy partners with Mondu to offer its IKEA Business Network members the MonduCard: Italian business customers can now apply for a Visa business credit card with 45-day deferred payment terms via Mondu, the Berlin-based B2B BNPL provider. The card itself is Mondu's product, used the same way at IKEA as at any other Visa-accepting merchant, making this more of a distribution partnership than a fully embedded card programme. (Mondu)

That's it for this edition. If you enjoy my newsletter, podcast, or events, the best way to support me is to share them with others in your network. Feedback is always welcome, too.

Need help with an embedded finance project? Visit my website and let's talk.

Best wishes from Berlin,

Lars Markull (LinkedIn)